Vibe Laundering, pt. 2: Citrini, the Co-Author and the Edit (remix not featuring the SEC)

Why language matters and words are powerful

Purple haze, all in my brain / Lately things they don’t seem the same / why has Citrini changed the authorship claim?

Hendrix’s “Purple Haze” sounds a bit off when you modify the lyrics like that, which just goes to show you that words have power, words disclose, and when those words sit on top of a report that moved hyperbolic billions in markets, what edits to it disclose might matter more than what the words originally said.

Since its publication, there have been material changes to the authorship claims on Citrini’s report, and these changes moved the co-author’s identity from a $262 million SEC-registered hedge fund to a friend with an idea. Interesting move considering that two days after publishing, the co-author (and fund’s managing partner) confirmed on Bloomberg Television that his firm held short positions in the companies the report named.

Read that again: the authorship attribution on a report attributed to market-moving was changed after publication, and the co-author is the managing partner of a $262 million SEC-registered hedge fund who confirmed short positions in the companies the report named.

I think this is worth examining, because it sits at the center of the vibe laundering architecture I mapped in Part 1 where the nature of disclosures and lack of transparency around positions sets the methodology for converting credibility into capital without rules around it or the content which it disseminates.

In part 2, I’ll examine who Alap Shah, the co-author of Citrini’s report is, what is and isn’t said about him, and why the changing of words for authorship are relevant. Then, I examine what the law says about all of it. In part 3 coming up after this, I evaluate three possible scenarios for what’s really happening chez Citrini in a work of speculative fiction of my own.

A necessary caveat before I continue (because I can go further, I promise, just like Kendrick): the February 23 selloff followed the Supreme Court striking down Trump’s tariffs along with Trump’s response and Anthropic’s news about modernizing COBOL systems, a two birds with one stone watershed moment rendering remaining difficult Boomer colleague(s) lording their knowledge genuinely unneeded forever (bye!) and, by the way also IBM fell 13%, its worst day since 2000. What I’m saying is the Citrini report was one element of a market that was already nervous, I’m not saying it caused the entire 821-point Dow decline. I am examining the disclosure architecture around one specific input and asking whether the regulatory framework accounts for it, because in vibe laundering, the structures which normally apply don’t and the rules which follow them seem non-existent.

Let me show you what I found.

I. Every breath you take, every edit you make, every move you make, the market’s watching you: changes in authorship for the Citrini report

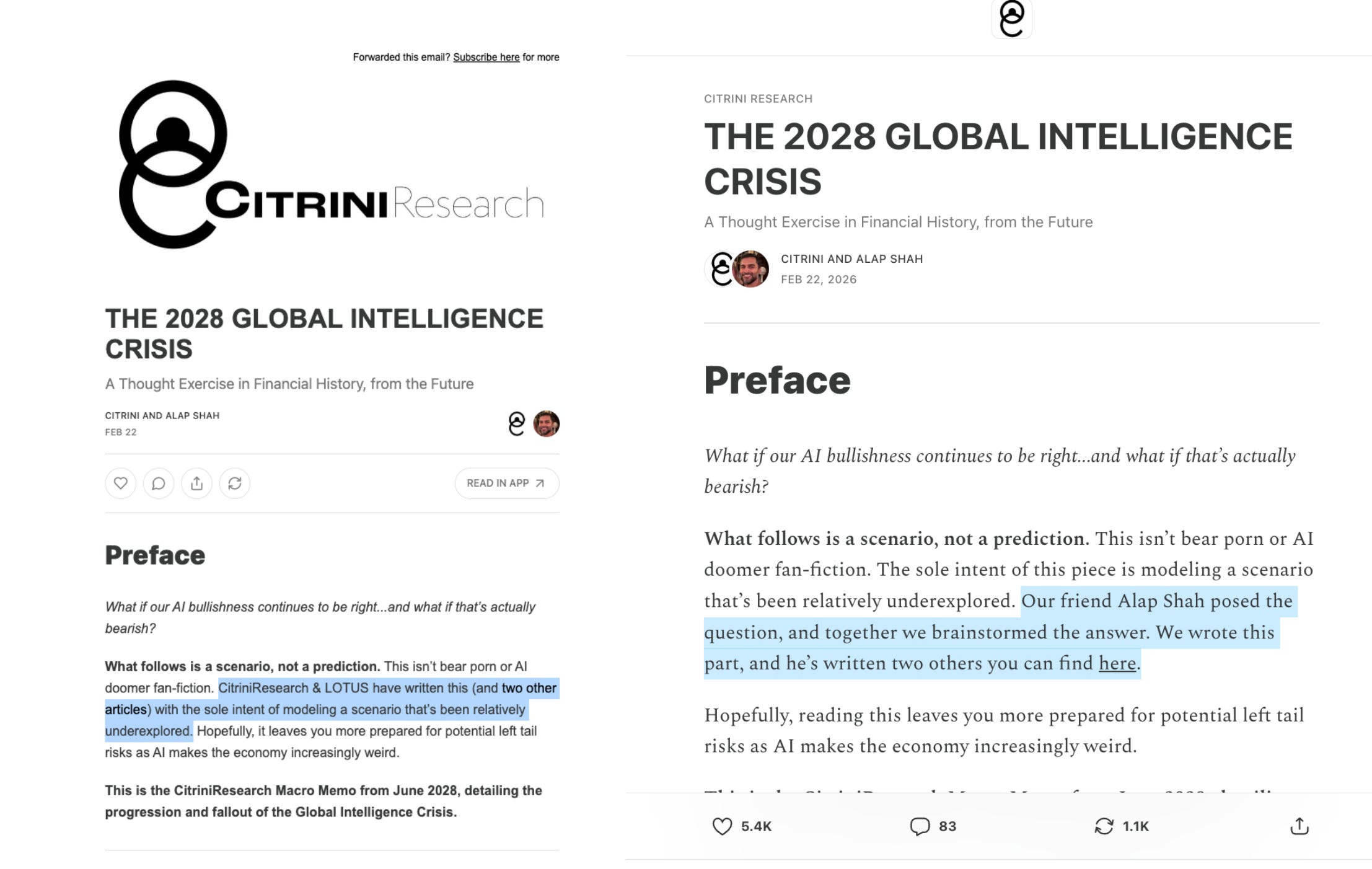

Recall on Sunday February 22, a Substack email from Citrini Research went out to 100k+ subscribers on a fictional memo from the future titled the 2028 Global Intelligence Crisis, and in the email, the preface identified the collaboration by stating plainly that “CitriniResearch & LOTUS have written this.” The man behind Lotus is attributed co-author Alap Shah, but what was not stated plainly anywhere at all on Citrini’s page is that LOTUS is Lotus Technology Management LP, an SEC-registered investment adviser managing $262 million. Timing wise, Shah, Lotus’ managing partner, filed a 13F with the SEC five days before the publication of the fictional memo showing $180 million in long equity. The Form ADV describes a long/short strategy with dedicated short selling, and two days after the report and the Dow moving 821 points, during an interview, Shah confirmed on Bloomberg Television that the firm held short positions in companies the report named.

That’s why the change in language around Shah and his role has been intriguing, as the version currently on Citrini’s website does not say “CitriniResearch & LOTUS have written this.”

It says “Our friend Alap Shah posed the question, and together we brainstormed the answer.”

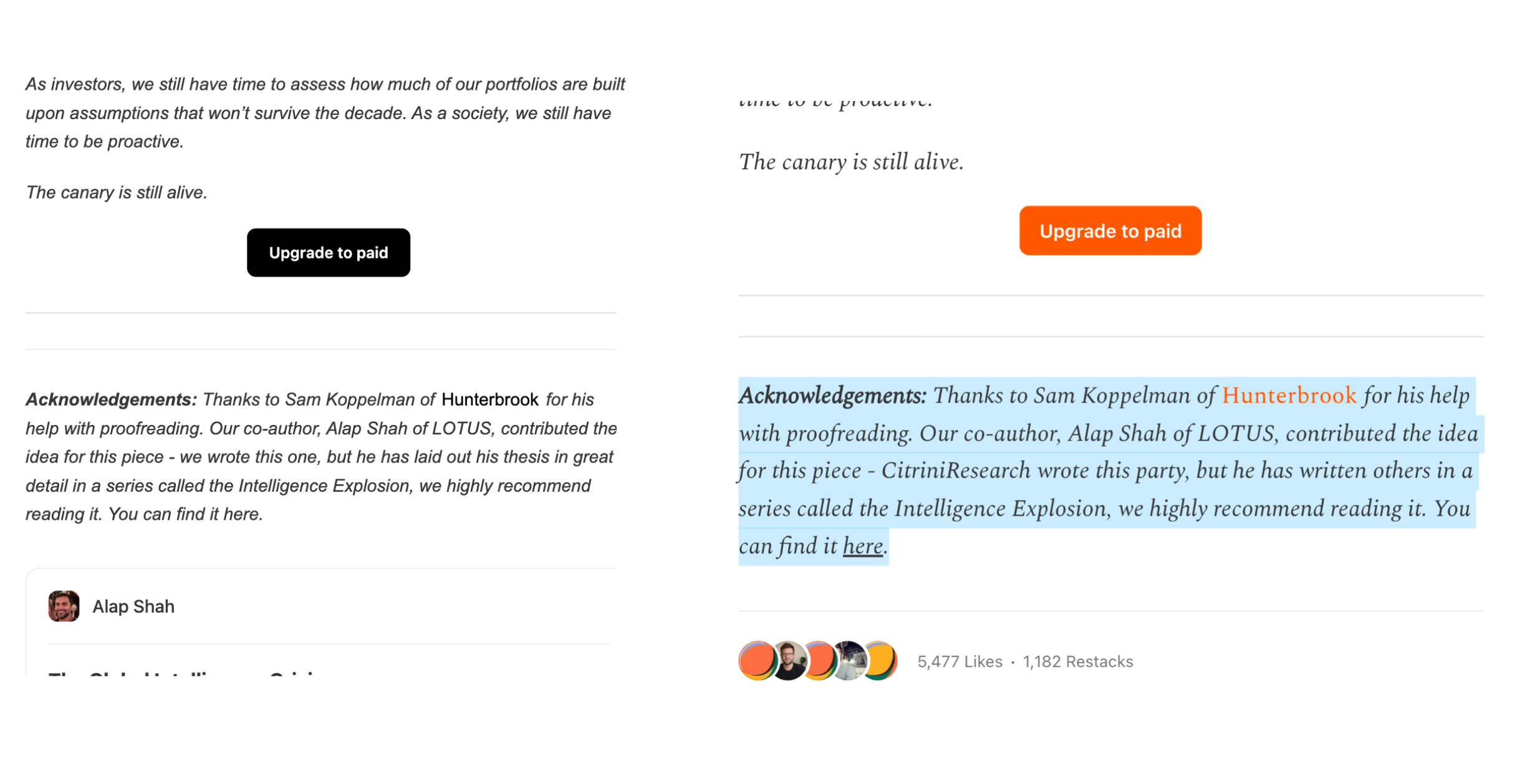

While it’s giving a little bit of “babe, they’re just a friend, don’t worry”, there’s more. The same directional shift in language for the pre-face appears in the acknowledgements. The original email sent to Citrini subscribers reads “Our co-author, Alap Shah of LOTUS, contributed the idea for this piece - we wrote this one.” Now, the website shows an edit to just saying “CitriniResearch wrote this party”

I assume this is a typo for “partly” though based on Citrini’s past with selling marijuana, I definitely believe he’d be fun to party with.

On the left, the original email, on the right, the website version now

Why is this all important? Remember how I said words have power? Substack emails are immutable, meaning the moment you originally hit publish on a post and elect to send it via email, it’s your only chance to send an email. Once the email goes out, you cannot edit it. But the website can be edited after. The version that reached every subscriber, the version they read and acted on before markets opened Monday, identified the collaboration as institutional without a disclosure or mention on Citrini’s website that LOTUS holds short positions on named assets mentioned in the fictional memo they authored. The version that exists now on the public web identifies it as personal.

What is happening here with words in the changes to the preface and acknowledgements appears to be editing that reduces the institutional footprint of the co-authorship, reframes an SEC-registered fund manager’s role from co-author to idea contributor, and all this occurs after the original publication reached subscribers’ inboxes as well as hyperbolic billions in market movements.

On the left, the original email, on the right, the website version now

In vibe laundering, disclosure and obligation are fluid depending on who does and says what where and when. So why would anyone change the specific wording on that only with relatively few to no other editorial changes in the overall fictional text?

II. The white lotus: who is Alap Shah & what is he saying

On the technical documentation front, Alap Shah is the Chief Investment Officer and Managing Partner of Lotus Technology Management LP, an investment advisory firm registered with the SEC since August 2025. The firm is also registered with the Cayman Islands Monetary Authority. Its CRD number is 335468 on the SEC’s Investment Adviser Public Disclosure database, and per Form ADV Part 2A, LOTUS has been registered with the SEC since August 2025 though having been in business since January 2024. It operates a master-feeder hedge fund structure: Lotus Technology Fund LP (domestic), Lotus Technology Offshore Fund LP (Cayman), and Lotus Technology Master Fund LP (Cayman).

On the professional experience front, Shah’s career runs through Viking Global, Citadel’s equities division, and the founding of Sentieo, an AI research platform acquired by AlphaSense in 2022. He is currently CEO of Littlebird, an AI personal assistant company whose stated business model involves AI agents performing tasks that human intermediaries currently perform, which is the central thesis of the report he co-authored.

Notice how the Citrini report said “Alap Shah of LOTUS” at the bottom? It does not identify Lotus Technology Management LP as an SEC-registered investment adviser managing $262 million. It does not disclose any positions held by the firm in companies named in the report. It does not disclose Shah’s role as CEO of Littlebird, a company whose business model is aligned with the report’s thesis that AI agents will displace human intermediaries.

The most charitable reading is straightforward and I’ll say it clearly: Shah may be one of the most qualified people in the country to write this fictional report given that he built and sold an AI company, runs a hedge fund focused on technology disruption, and is building another AI company. The report may be good analysis from someone who understands the technology better than most. His positions may reflect conviction, not a scheme. All of that can be true. My question is narrower. When an SEC-registered investment adviser co-authors market-moving research on a third-party platform, what are the disclosure obligations, and were they met?

On Shah’s own Substack, published the same day, there is a general directional disclosure,”Because I see this AI-driven displacement as a likely path, my portfolios and companies are positioned for it. If my thesis plays out, my firms will benefit financially.” That post received 289 likes. The Citrini report received 5,477 likes, 1,182 restacks, and was read by sixteen million people. That means Citrini’s report got 19x the distribution and exposure to readers, rendering the disclosure gap between those two platforms at minimum wide.

Lotus’s Form ADV Part 2A does not reference Littlebird, does not reference any arrangement for co-authoring research on third-party platforms, and describes its long/short strategy in generic terms. Shah co-authored a report arguing AI agents will displace human intermediaries. He runs an AI agent company. He runs a hedge fund that holds short positions in the companies being disrupted. Whether or not Littlebird fits into a specific ADV line item, the interconnection between these roles is the kind of conflict that fiduciary duty exists to surface. It’s also the sort of thing that vibe laundering describes happening - you know it when you see it though you can’t exactly place a name on it.

III. Lucky number 13F - what the form shows, cannot show, and how this ties into Shah admitting to holding short positions on television

As mentioned, five days before the Citrini report was published, Lotus filed their form 13F-HR with the SEC This appears to be the firm’s first 13F filing, was signed by Shah as CIO, and it reports 147 long equity positions totaling approximately $180 million in market value.

A 13F reports long equity positions. It does not report short positions. This is not a gap unique to Lotus as it applies to everyone for Form 13F.

The portfolio includes positions in companies the report named, including Uber ($1.50 million), and in companies within sectors the report thematically targeted as vulnerable to AI disruption: MongoDB ($281,000), Cloudflare ($358,000), CrowdStrike ($208,000), Twilio ($700,000), Etsy ($2.24 million), Coinbase ($204,000)

If you do the math, the firm’s Form ADV reports $262 million in regulatory assets under management. The 13F reports approximately $180 million in long equity. The difference, approximately $82 million, represents positions that 13F filings are not designed to capture i.e. in short sales, derivatives, private investments, cash, and non-US securities.

The 13F also shows that Lotus held long positions in Uber and MongoDB as of December 31, 2025, and both companies were named in the report as vulnerable to AI disruption in addition to declining on February 23. This means Lotus lost money on those long positions because of the report its managing partner co-authored. I think it is fair to say a fund running a pure short-and-distort scheme does not hold longs in the companies it is trying to drive down. The long positions are consistent with a fund that holds a genuinely mixed view, going long on the companies it thinks will adapt, short the ones it thinks won’t, and publishing analysis that reflects a thesis rather than a trade.

As of writing, there is no public filing in the United States that reveals which investment manager holds which short position. The rule designed to change this, Rule 13f-2 and Form SHO, has been delayed to January 2028. No manager has ever filed a Form SHO. FINRA collects aggregate short interest data per security, but this shows only total shares shorted, not who is shorting.

The practical consequence of this is that positions most likely to benefit from market-moving bearish research are positions the current disclosure system was not built to reveal.

Keeping this in mind (and I don’t even go into how Shah brings up his thesis in detail in various places), two days after the fictional memo went out and the Dow dropped 821 points, Shah appeared on Bloomberg Television, stating that his firm “certainly had shorts in some of these businesses” and that they “generally have a set of shorts out against businesses that we think are going to be disrupted by AI.” That means Shah confirmed the short positions on television after the market moved. It’s the only reason why the public knows about Lotus’s short positioning, as no filing nor regulation required it. Shah offered this information upon being asked about it.

Shah also stated “I thought there was going to be a small reaction. It was definitely larger than we expected.”

When the interviewer asked directly whether this was “a short seller report guised beautifully in the form of a beautiful fiction,” Shah did not say no. He said “We are constantly sort of turning our book. And we certainly had shorts in some of these businesses.” The question was about the report’s intent, but the answer was about the portfolio’s composition, and this distance between appears in the edits to the attribution of the report in the first section.

The original email named the fund, but now on the website where the report lives, it names a friend. It’s just like how the Bloomberg answer acknowledges the shorts but frames them as routine portfolio management rather than positioned exposure behind a specific publication. Words are power, power is in disclosure, and in both cases, the words used to describe the relationship between the fund and the report narrows after the fact. The edits narrow the authorship as the interview narrows the intent. Now it’s giving “Babe, they’re just a friend - I swear!”

Vibe laundering means none of this is required or planned, of course. It is entirely possible that every edit and every answer reflects nothing more than normal post-publication clarification and honest interviewing to the extent a reporter at Bloomberg views it to be part of their job. The direction of the narrative and its framing is consistent since by the time the public record settles, the fund’s connection to the report is smaller under possible scrutiny than it was when the report first hit inboxes.

Words have power, so consider this. Shah told us in his own words he anticipated market impact from the report. He published it with no per-report position disclosure on the platform where sixteen million people read it. The specific positions were confirmed publicly only after the trading session was over. It was a fictional report that he anticipated market impact from.

I want to be fair about what that means - Shah disclosed directionally on his own Substack on publication day and his short positions on TV. Not everyone would do that, of course, but the question is not whether Shah acted in bad faith. It is whether voluntary after-the-fact disclosure on a different platform satisfies the obligations the SEC has articulated for registered investment advisers, and whether the point of market impact, not the point of television appearance, is where those obligations attach.

I also want to note that at 8:33 AM on February 23, before the market opened, the @lotusaifund Twitter account, the fund’s official account, promoted both Shah’s solo Substack piece and the Citrini collaboration. That means the fund was promoting the research that the author anticipated would have some sort of reaction per Shah’s Bloomberg interview. The disclosure on Shah’s own post (”my portfolios and companies are positioned for it”) existed on his platform, but again, it did not exist on the platform the fund was directing people to read.

V. I am the law: what legal precedents exist about vibe laundering

Say it with me - words are: powerful. Consider how there is a difference between deception, omission, and influence. Legal questions are precise even when answers are not, and to be clear, I am not making legal conclusions. I am describing what the law around markets says and what has happened in the past for situations as precedents.

The strongest precedent is SEC v. Capital Gains Research Bureau from 1963, when the Supreme Court held that an investment adviser’s failure to disclose a personal interest in securities being recommended constituted fraud under the Advisers Act. The Court did not require proof of intent to injure or that clients actually lost money as the existence of the undisclosed conflict was sufficient. It seems that post-publication revision of attribution language on a market-moving report, which shifts from institutional co-authorship to personal friendship, is the kind of evidence this framework may have been designed to evaluate.

Decades later, the SEC’s 2019 Commission Interpretation, Release No. IA-5248, stated that disclosure must be “sufficiently specific so that a client is able to understand the material fact or conflict of interest.” The Commission stated that an adviser that discloses it “may” have a conflict when one actually exists has not provided adequate disclosure. Accordingly, a site-wide Terms of Service page stating team members “may have existing long or short positions” is the definition of disclosing that a conflict “may” exist, but the SEC has said that is not enough.

The most directly analogous enforcement action is In re Anson Funds Management, Release No. 6622, June 2024. In this case, the SEC charged Anson Funds for failing to disclose their collaboration with activist short publishers. The fund described its short strategy in generic terms but did not disclose that it involved working with short publishers, trading around publication, and sharing profits. The SEC found these omissions rendered the fund’s disclosures misleading and the combined penalty was $2.25 million.

Now, besides the fact that this is a speculative work of fiction (while keeping in mind what is known and said about it by its authors), there are important distinctions to these precedents. Anson involved profit-sharing arrangements and advance access to research and there is no public evidence of such arrangements between Lotus and Citrini. The question is not whether Shah deceived anyone (besides, it’s fiction, etc.). The question is instead under what standards the SEC has articulated in the past whether the disclosure was adequate at the point of market impact, and whether co-authoring research on a third-party platform with no disclosure architecture, then revising the attribution language after publication, constitutes an omission of the type the Advisers Act addresses.

Whether the Anson framework applies to a situation where a principal SEC registered fund manager co-authors research for a fictional speculative work on a third-party platform, rather than working with a short publisher in a formal arrangement, is an open question. The SEC has not addressed this specific scenario in any published guidance, enforcement action, or no-action letter I have been able to identify.

I do not have the answer, as I am just identifying what the law says and what happened.

One further note - the publisher exclusion under Lowe v. SEC protects ‘bona fide’ publications containing ‘disinterested commentary.’ Whether a fictional speculative report co-authored by an SEC-registered fund manager holding short positions in the named companies qualifies as ‘disinterested’ is a question the courts have not yet been asked to answer.

It’s a watershed moment for vibe laundering in many ways including coining the term (I want my Urban Dictionary credit, damnit).

Part 3 of the vibe laundering series, which is the speculative memo from the future, comes out soon.

Great investigation and amazing article.

Interesting to read!