What 118K followers & 100 hours gets you - rewriting Citrini's 2028 Global Intelligence crisis report, but make it good

What happens when you tell a financial figure with 118,000 followers that his 5,000-word AI crisis piece has good research but the writing reads like AI even though it isn't?

He blocks you.

So I did the rewrite anyway.

Some selected blocks from Citrini’s original report side by side with my rewrites as a case study, for the love of the game, and simply because it is fun to challenge oneself and grow to become a better writer. You can have the best research in the world, you can have all of the intel, but substance and style are a never-ending project. Sometimes the sycophantic echoes slow you down in your growth.

Citrini’s original - Block 1:

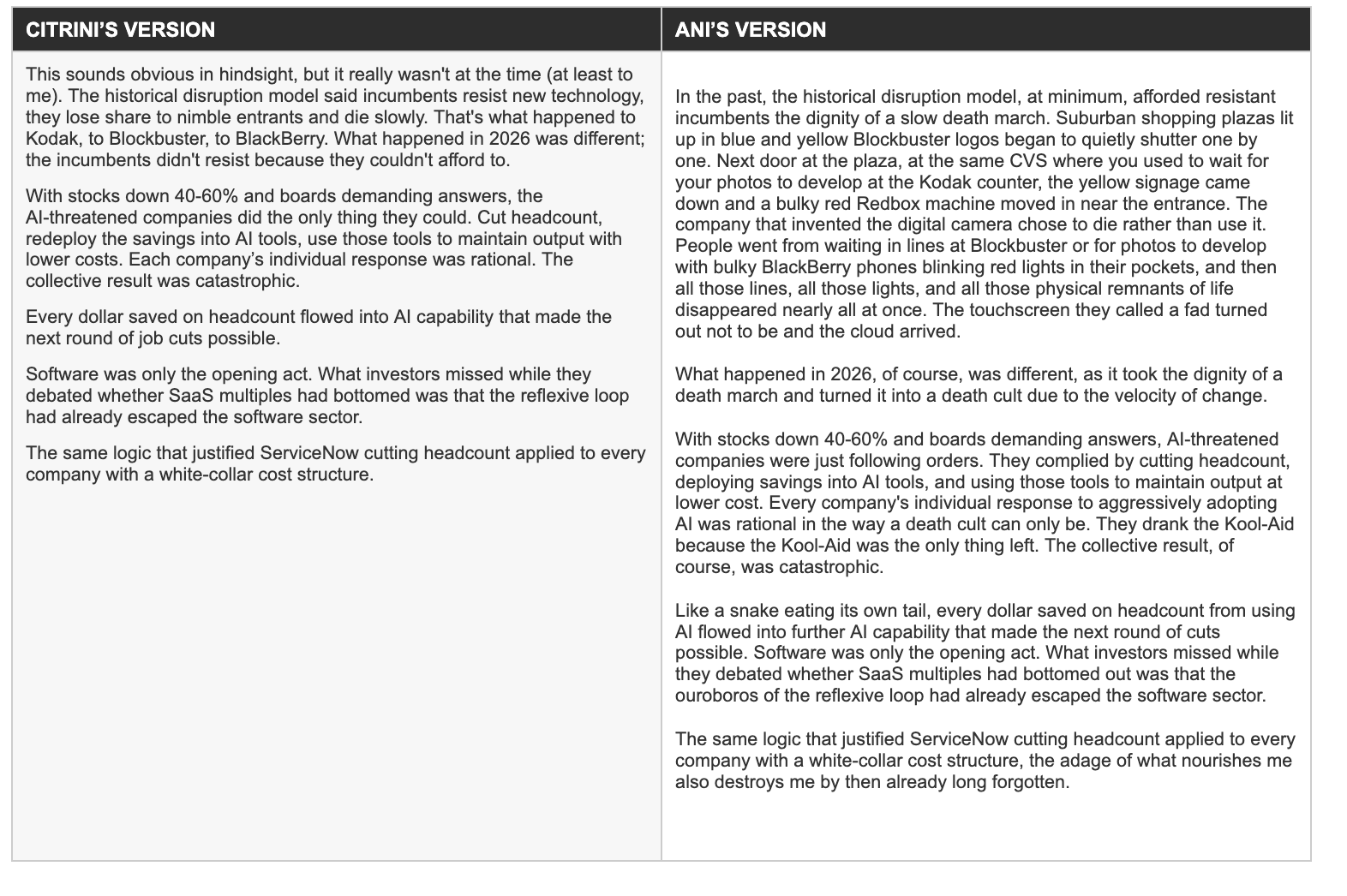

This sounds obvious in hindsight, but it really wasn’t at the time (at least to me). The historical disruption model said incumbents resist new technology, they lose share to nimble entrants and die slowly. That’s what happened to Kodak, to Blockbuster, to BlackBerry. What happened in 2026 was different; the incumbents didn’t resist because they couldn’t afford to.

With stocks down 40-60% and boards demanding answers, the AI-threatened companies did the only thing they could. Cut headcount, redeploy the savings into AI tools, use those tools to maintain output with lower costs.

Each company’s individual response was rational. The collective result was catastrophic. Every dollar saved on headcount flowed into AI capability that made the next round of job cuts possible.

Software was only the opening act. What investors missed while they debated whether SaaS multiples had bottomed was that the reflexive loop had already escaped the software sector. The same logic that justified ServiceNow cutting headcount applied to every company with a white-collar cost structure.

My rewrite:

In the past, the historical disruption model, at minimum, afforded resistant incumbents the dignity of a slow death march. Suburban shopping plazas lit up in blue and yellow Blockbuster logos began to quietly shutter one by one. Next door at the plaza, at the same CVS where you used to wait for your photos to develop at the Kodak counter, the yellow signage came down and a bulky red Redbox machine moved in near the entrance. The company that invented the digital camera chose to die rather than use it. People went from waiting in lines at Blockbuster or for photos to develop with bulky BlackBerry phones blinking red lights in their pockets, and then all those lines, all those lights, and all those physical remnants of life disappeared nearly all at once. The touchscreen they called a fad turned out not to be and the cloud arrived.

What happened in 2026, of course, was different, as it took the dignity of a death march and turned it into a death cult due to the velocity of change.

With stocks down 40-60% and boards demanding answers, AI-threatened companies were just following orders. They complied by cutting headcount, deploying savings into AI tools, and using those tools to maintain output at lower cost. Every company’s individual response to aggressively adopting AI was rational in the way a death cult can only be. They drank the Kool-Aid because the Kool-Aid was the only thing left. The collective result, of course, was catastrophic.

Like a snake eating its own tail, every dollar saved on headcount from using AI flowed into further AI capability that made the next round of cuts possible. Software was only the opening act. What investors missed while they debated whether SaaS multiples had bottomed out was that the ouroboros of the reflexive loop had already escaped the software sector.

The same logic that justified ServiceNow cutting headcount applied to every company with a white-collar cost structure, the adage of what nourishes me also destroys me by then already long forgotten.

Citrini’s original - Block 2:

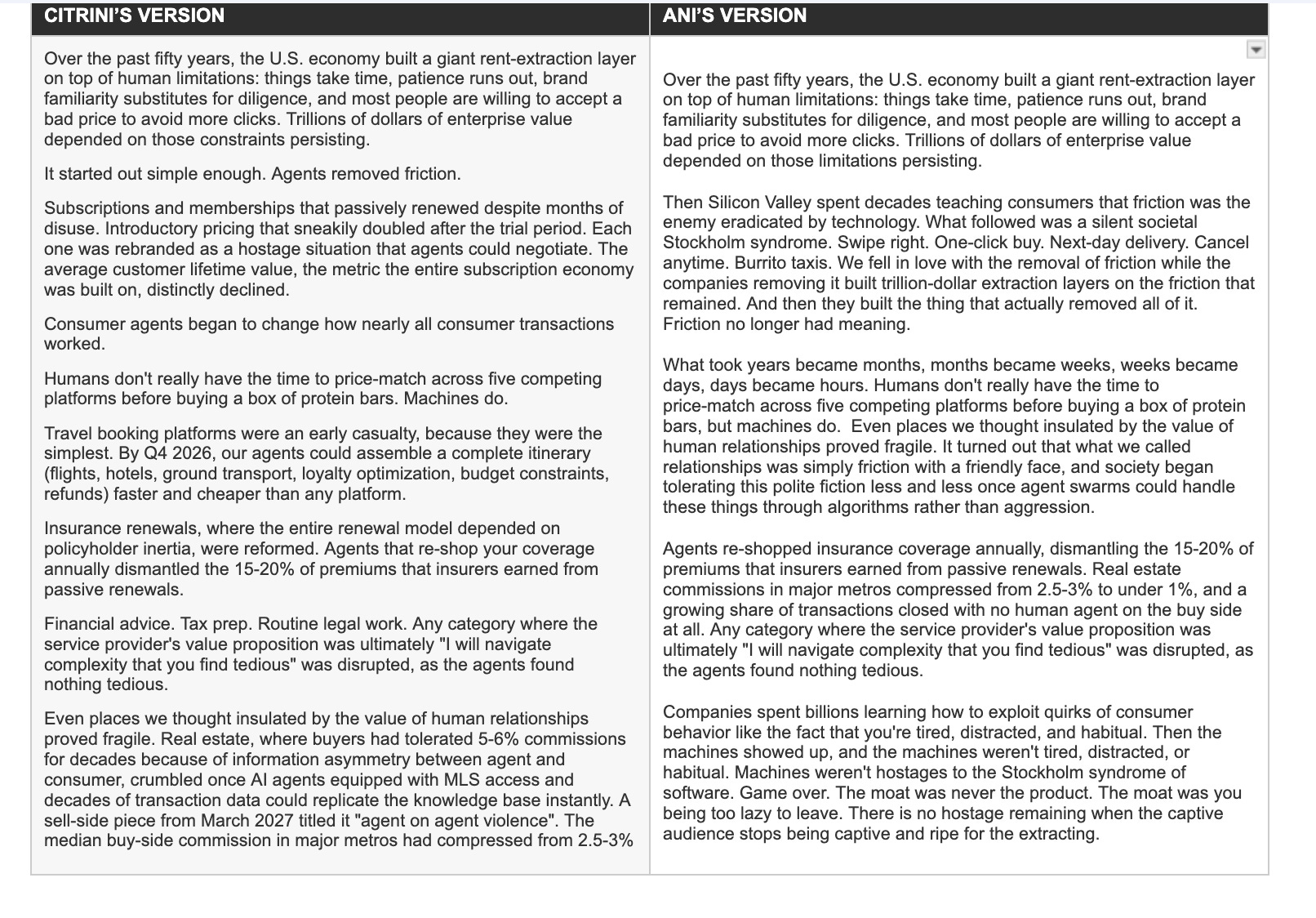

Over the past fifty years, the U.S. economy built a giant rent-extraction layer on top of human limitations: things take time, patience runs out, brand familiarity substitutes for diligence, and most people are willing to accept a bad price to avoid more clicks. Trillions of dollars of enterprise value depended on those constraints persisting.

It started out simple enough. Agents removed friction.

Subscriptions and memberships that passively renewed despite months of disuse. Introductory pricing that sneakily doubled after the trial period. Each one was rebranded as a hostage situation that agents could negotiate. The average customer lifetime value, the metric the entire subscription economy was built on, distinctly declined.

Consumer agents began to change how nearly all consumer transactions worked.

Humans don’t really have the time to price-match across five competing platforms before buying a box of protein bars. Machines do.

Travel booking platforms were an early casualty, because they were the simplest. By Q4 2026, our agents could assemble a complete itinerary (flights, hotels, ground transport, loyalty optimization, budget constraints, refunds) faster and cheaper than any platform.

Insurance renewals, where the entire renewal model depended on policyholder inertia, were reformed. Agents that re-shop your coverage annually dismantled the 15-20% of premiums that insurers earned from passive renewals.

Financial advice. Tax prep. Routine legal work. Any category where the service provider’s value proposition was ultimately “I will navigate complexity that you find tedious” was disrupted, as the agents found nothing tedious.

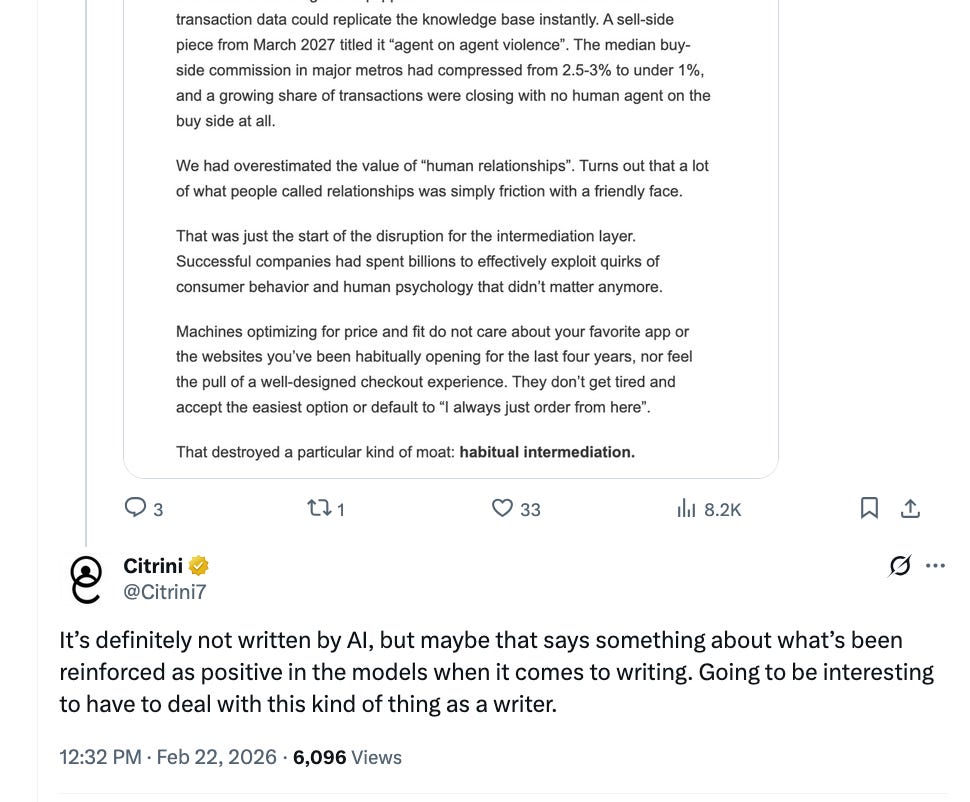

Even places we thought insulated by the value of human relationships proved fragile. Real estate, where buyers had tolerated 5-6% commissions for decades because of information asymmetry between agent and consumer, crumbled once AI agents equipped with MLS access and decades of transaction data could replicate the knowledge base instantly. A sell-side piece from March 2027 titled it “agent on agent violence”. The median buy-side commission in major metros had compressed from 2.5-3% to under 1%, and a growing share of transactions were closing with no human agent on the buy side at all.

We had overestimated the value of “human relationships”. Turns out that a lot of what people called relationships was simply friction with a friendly face.

That was just the start of the disruption for the intermediation layer. Successful companies had spent billions to effectively exploit quirks of consumer behavior and human psychology that didn’t matter anymore.

Machines optimizing for price and fit do not care about your favorite app or the websites you’ve been habitually opening for the last four years, nor feel the pull of a well-designed checkout experience. They don’t get tired and accept the easiest option or default to “I always just order from here”.

That destroyed a particular kind of moat: habitual intermediation.

My rewrite:

Over the past fifty years, the U.S. economy built a giant rent-extraction layer on top of human limitations: things take time, patience runs out, brand familiarity substitutes for diligence, and most people are willing to accept a bad price to avoid more clicks. Trillions of dollars of enterprise value depended on those limitations persisting.

Then Silicon Valley spent decades teaching consumers that friction was the enemy eradicated by technology. What followed was a silent societal Stockholm syndrome. Swipe right. One-click buy. Next-day delivery. Cancel anytime. Burrito taxis. We fell in love with the removal of friction while the companies removing it built trillion-dollar extraction layers on the friction that remained. And then they built the thing that actually removed all of it. Friction no longer had meaning.

What took years became months, months became weeks, weeks became days, days became hours. Humans don’t really have the time to price-match across five competing platforms before buying a box of protein bars, but machines do.

Even places we thought insulated by the value of human relationships proved fragile. It turned out that what we called relationships was simply friction with a friendly face, and society began tolerating this polite fiction less and less once agent swarms could handle these things through algorithms rather than aggression.

Agents re-shopped insurance coverage annually, dismantling the 15-20% of premiums that insurers earned from passive renewals. Real estate commissions in major metros compressed from 2.5-3% to under 1%, and a growing share of transactions closed with no human agent on the buy side at all. Any category where the service provider’s value proposition was ultimately “I will navigate complexity that you find tedious” was disrupted, as the agents found nothing tedious.

Companies spent billions learning how to exploit quirks of consumer behavior like the fact that you’re tired, distracted, and habitual. Then the machines showed up, and the machines weren’t tired, distracted, or habitual. Machines weren’t hostages to the Stockholm syndrome of software. Game over. The moat was never the product. The moat was you being too lazy to leave. There is no hostage remaining when the captive audience stops being captive and ripe for the extracting.

Citrini’s original - Block 3:

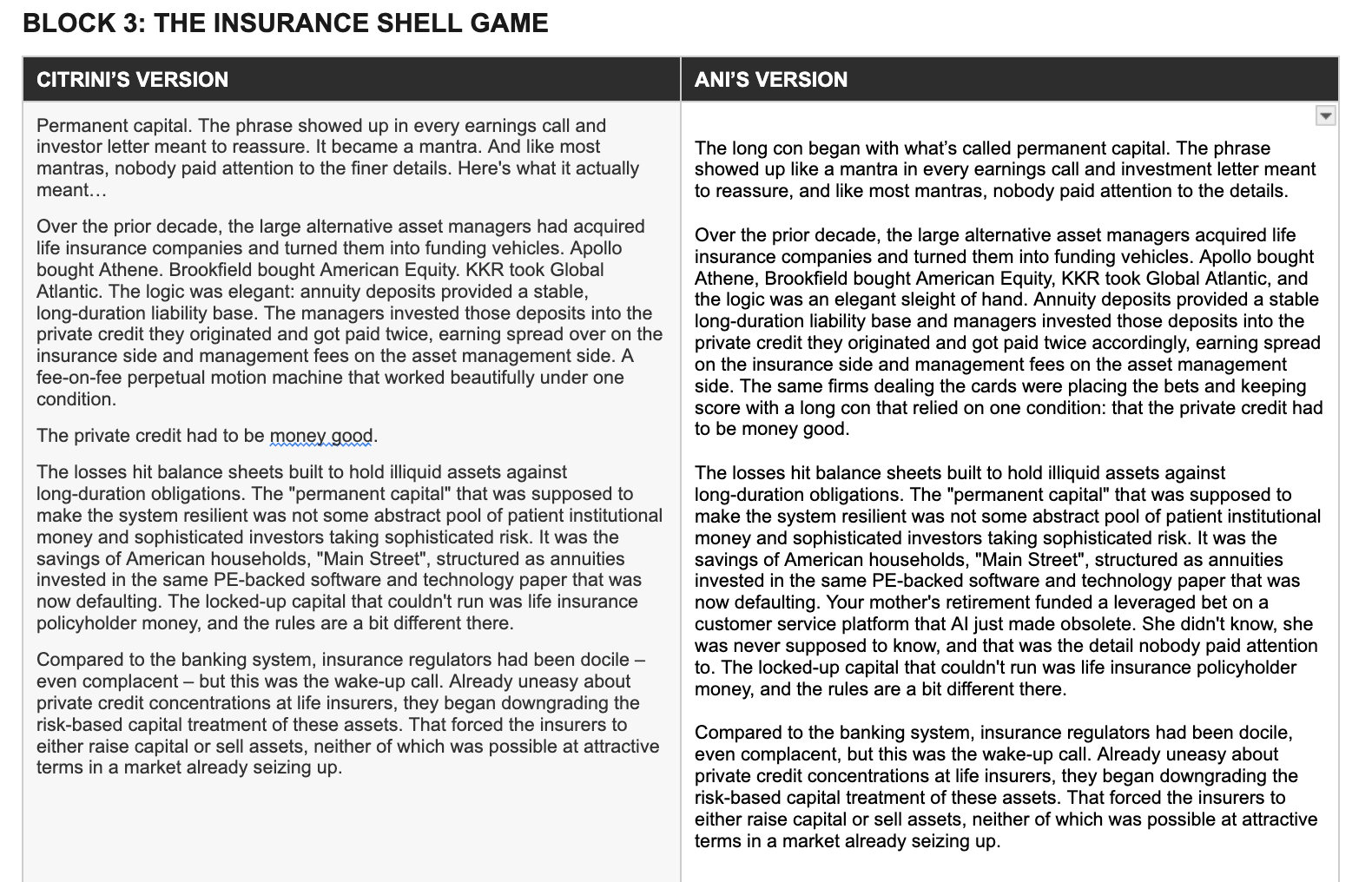

Permanent capital. The phrase showed up in every earnings call and investor letter meant to reassure. It became a mantra. And like most mantras, nobody paid attention to the finer details. Here’s what it actually meant…

Over the prior decade, the large alternative asset managers had acquired life insurance companies and turned them into funding vehicles. Apollo bought Athene. Brookfield bought American Equity. KKR took Global Atlantic. The logic was elegant: annuity deposits provided a stable, long-duration liability base. The managers invested those deposits into the private credit they originated and got paid twice, earning spread over on the insurance side and management fees on the asset management side. A fee-on-fee perpetual motion machine that worked beautifully under one condition.

The private credit had to be money good.

The losses hit balance sheets built to hold illiquid assets against long-duration obligations. The “permanent capital” that was supposed to make the system resilient was not some abstract pool of patient institutional money and sophisticated investors taking sophisticated risk. It was the savings of American households, “Main Street”, structured as annuities invested in the same PE-backed software and technology paper that was now defaulting. The locked-up capital that couldn’t run was life insurance policyholder money, and the rules are a bit different there.

Compared to the banking system, insurance regulators had been docile - even complacent - but this was the wake-up call. Already uneasy about private credit concentrations at life insurers, they began downgrading the risk-based capital treatment of these assets. That forced the insurers to either raise capital or sell assets, neither of which was possible at attractive terms in a market already seizing up.

My rewrite:

The long con began with what’s called permanent capital. The phrase showed up like a mantra in every earnings call and investment letter meant to reassure, and like most mantras, nobody paid attention to the details.

Over the prior decade, the large alternative asset managers acquired life insurance companies and turned them into funding vehicles. Apollo bought Athene, Brookfield bought American Equity, KKR took Global Atlantic, and the logic was an elegant sleight of hand. Annuity deposits provided a stable long-duration liability base and managers invested those deposits into the private credit they originated and got paid twice accordingly, earning spread on the insurance side and management fees on the asset management side. The same firms dealing the cards were placing the bets and keeping score with a long con that relied on one condition: that the private credit had to be money good.

The losses hit balance sheets built to hold illiquid assets against long-duration obligations. The “permanent capital” that was supposed to make the system resilient was not some abstract pool of patient institutional money and sophisticated investors taking sophisticated risk. It was the savings of American households, “Main Street”, structured as annuities invested in the same PE-backed software and technology paper that was now defaulting. Your mother’s retirement funded a leveraged bet on a customer service platform that AI just made obsolete. She didn’t know, she was never supposed to know, and that was the detail nobody paid attention to. The locked-up capital that couldn’t run was life insurance policyholder money, and the rules are a bit different there.

Compared to the banking system, insurance regulators had been docile, even complacent, but this was the wake-up call. Already uneasy about private credit concentrations at life insurers, they began downgrading the risk-based capital treatment of these assets. That forced the insurers to either raise capital or sell assets, neither of which was possible at attractive terms in a market already seizing up.

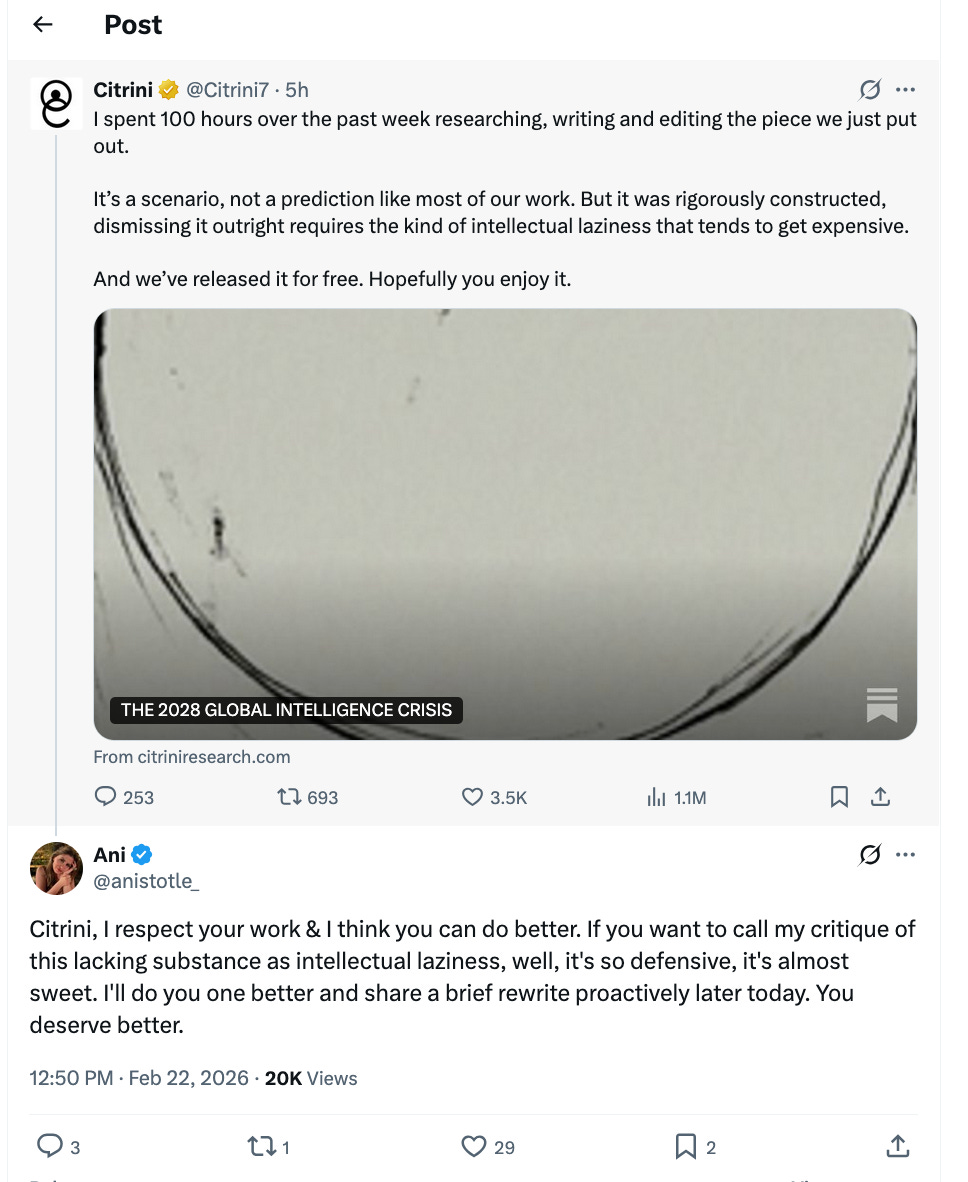

What does rewriting Citrini’s 2028 report show us?

I’ll be upfront: I only rewrote three blocks because I have better things to do, such as petting the cat on my lap. The other blocks can consider this a professional courtesy.

The research is his. It's good research. It has good ideas. But finding and having the information is never the hardest part, though it is tedious and requires effort - making someone feel it is. He spent 100 hours writing a piece about the end of the world and even though it isn’t AI, it reads like in parts and structures. At best, you can attempt to advance that AI is calibrating for writing like this. At worst, I’ll let you fill in the blanks. But there’s something far more interesting going on here than a fintwit beef over an opinion on style: what do we consider substance, what is style, and what are our standards for good taste, engagement, and intellectual honesty in the era of AI slop? My rewrites reflect what I think involves a kind of narrative cohesion, cadence, and care for the topic that reflects a through-line between the theme and the narrative of it. That being said, someone reading this could think my writing is garbage, Citrini’s is better, or that Citrini’s writing is garbage, mine’s is better, or that efinancialcareers.com is the best, we are both mid, etc. It isn’t about what is better or best or be best as our First Lady would say. It is about the love of the game and using one’s brain to be true to it. All of this being an intriguing exercise for an otherwise sleepy Sunday, I’ll end it on this note - intriguingly, Citrini offered of his own volition the following comments.

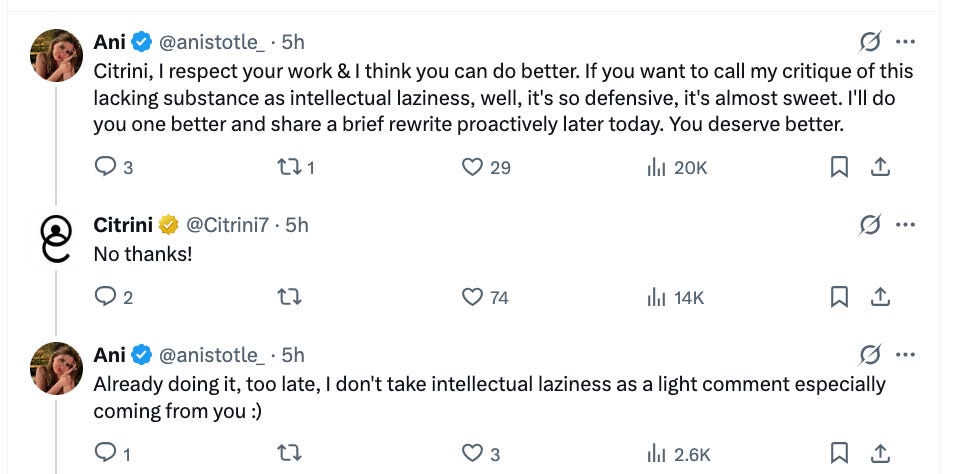

According to Citrini, 'dismissing it outright requires intellectual laziness that tends to get expensive.' This was in his original post, before I ever commented. He set the terms: critique equals laziness. Obviously I didn't dismiss it, but Citrini tells himself one story that makes a critique about the form of the writing from an unknown writer palatable and then blocks me for offering the rewrite. Professional decorum and standards of judgement are fluid, but blocking a 2,000-follower account for engaging seriously with your work through a rewrite that reflects your own ideas and research is not the flex of a man confident in his craft.

If these are the standards of intellectual honesty in our community, we should probably rewrite those too.

You can decide which version you'd rather read to the end. I just think intellectual honesty requires engaging with something rather than shutting it down. Disappointing from a fellow Bruin. But he is sure I’m the better writer, so based on him being sure about how things are, I won’t question the logic.

Timeline of posts:

1. My original post at 11:48am this morning after my initial read of the report with Citrini’s two replies at 12:32pm questioning what the future is for writers and then showing all his cards on critique:

2. Less than 30 minutes after my original post, Citrini’s post at 12:25pm reflecting the vast wound of intellectual laziness:

The style debate is fun but kind of beside the point. This piece moved markets. Not because the writing was good or bad, but because someone wrote a specific future down in enough detail that people acted on it. That's the part worth paying attention to.

No offense but, I don't think your rewrite added anything. The original post was clear and communicated his point. Your rewrite is a different style but, doesn't communicate it better. I find his writing clearer and more to the point. You've added more stylistic prose but, this is an economic analysis not a novel.

It just feels like you're making an almost meaningless critique of piece that actually did go viral and did move the markets so, it clearly communicated to its audience.